Overnight Snapshot

The Day Ahead

0900hrs UK EU EuroZone Current Account (previous €37.6bln SA/€12.8bln NSA)

0930hrs UK UK Retail Sales Ex Auto Fuel (est -0.45%mom/1.38%yoy vs previous 0.6% / 1.1%)

0930hrs UK UK Retail Sales Inc Auto Fuel (est -0.7%mom/1.9%yoy vs previous 0.8%/1.5%)

1110hrs UK UK Bank of England Policy Maker Alex Brazier speaks at Imperial College, London

1300hrs UK US Fed Governor Lael Brainard speaks in Washington

1330hrs UK US Weekly Jobless Claims (est 229K vs previous 233K)

1330hrs UK US Philadelphia Fed Business Outlook (est 20.8 vs previous 22.3)

1430hrs UK US Fed Governor and Vice Chair for Bank Supervision Randal Quarles gives semi annual testimony before Senate Banking Committee

1500hrs UK US Leading Indicators (est 0.3% vs previous 0.6%)

1700hrs UK NO Norges Bank Governor Olsen speaks in Oslo

1730hrs UK UK Bank of England’s Jon Cunliffe speaks in Washington

1815hrs UK NO Norges Bank Deputy Governor Jon Nicolaisen speaks in Philadelphia

2345hrs UK US Cleveland Fed President Loretta Mester speaks at the University of Pittsburgh

FTSE100 ex dividend 9.789 points today (BAE, Barrat Dev, Croda, Informa, Lloyds, Standard Life)

US earnings releases today include Blackstone Group, Procter & Gamble, Snap-On, Bank of New York Mellon, Philip Morris, and Alliance Data Systems

The Day So Far….

STOCKS: The S&P500 carved out a small gain as the Dow dipped after a volatile session with weakness in Consumer Staples and Financials offset against gains in Energy and Industrials. However, IBM caused a heavy drag on the S&P, falling7.5% as quarterly profits bucked the trend and disappointed. The Dow closed down 38.56 at 24748.07, the S&P500 added 2.25 points to finish at 2708.64, whilst the tech based Nasdaq100 moved up 16.844 points to close 6833.213

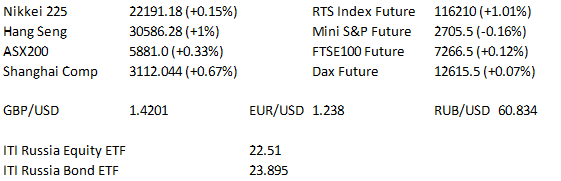

The major Asia-Pacific indices have traded in the green as a continued pull back in volatility measures allowed the space to push higher. - The Nikkei 225 posted solid gains of close to 1% in early trade as the materials sector charged higher, although the consumer sectors limited the index's scope for gains and much of the increase was eroded as the day wore on. - Hong Kong's Hang Seng added nearly 1.6%, with the energy sector leading the way, with all 9 major sectors posting gains early on, although as in Japan some gains being eroded as we approach the close. The mainland Shanghai Composite added 1.00% and seems steady in late trade - Australia's ASX 200 logged gains of 0.5% as the heavyweight material sector underpinned the index, although telecoms & IT provided the largest drags and the Index eased back to gains of around 0.3% before trading sideways for the last couple of hours.

OIL: Crude pushed higher as risk sentiment was buoyant in the Asia-Pacific session. WTI & Brent added $0.40-0.50 to trade at $68.90 & $ 74.00 respectively. - This came after the latest round of US DoE inventory data (released Wednesday), which pointed to a fall in inventories across the board.

US TSYS: The space was dragged away from session lows on the back of a softer than expected Australian labour market report, although T-Note futures have stuck to a 3 tick range thus far. - The Tsy curve has undergone a modest degree of bull flattening in Asia, although price action has been somewhat limited. -

The Eurodollar strip is mainly higher with the white and red contracts unchanged to a tick better off.

GOLD: Gold added $3 to trade at $1352/oz (around 0.25% up) to post gains of 0.4% on the week. Holdings in ETF’s backed by Gold rose for the 11th straight day on Wednesday, to the highest level since 2013, according to data compiled by Bloomberg. Palladium also trading strongly, heading for it’s best winning streak since June and up around 15% since April 6th when the US hit aluminium producer Rusal with sanctions

FOREX: AUDUSD moved to session lows on the back of a soft Aussie labour market report & as the prior report was revised lower, hitting a low of 0.7764, before sharply reversing to last deal at ~0.7790, with little in the way of fundamental headlines since the release, although iron ore & copper prices are higher. – NZD popped higher on the back of the slightly better than exp. New Zealand CPI print. Earlier on RBNZ Gov. Orr noted that the RBNZ "expects very benign inflation going forwards." Orr went on to say that "what really matters is the confidence and expectation and belief that we are aiming for that midpoint of 2%

all the time." After easing back to session lows NZDUSD last trades relatively unchanged at 0.7325. - JPY crosses have moved higher as equities ticked up & the Trump-Abe summit delivered a warmer tone re: trade, although both leaders are seemingly sticking to their original stances. USDHKD cross saw a degree of profit taking as the HKMA tried to instill a sense of calm. EURUSD stuck to a tight range with a notable amount of FX option expiries in play between 1.2300 & 1.2400

For information on ITI ETFs contact Elio Manca

For institutional sales & trading please contact Steve Farrell

For all dealing enquiries please contact our Trading Desk