Overnight Snapshot

The Day Ahead

0930hrs UK Bank of England MPC Meeting Minutes Released

1030hrs UK ECB Governing Council Member Jens Weidmann Speaks In Vienna

1100hrs UK Riksbank Deputy Governor Cecilia Skingsley speaks in Sodertalje

1400hrs UK ECB’s Nouy speaks in Brussels

1430hrs UK Dallas Fed Manufacturing Index (est 31.5 vs previous 37.2)

1730hrs UK New York Fed President William Dudley speaks on Financial Regulation in Washington

2130hrs UK Cleveland Fed President Loretta Mester speaks on monetary policy at Princeton University

The Day So Far….

STOCKS: Political tension seems to have replaced interest rates as the #1 worry on Wall Street as increasing concerns over trade wars dominate. The continuing hiring/firing of the top advisers at the White House does not help. US shares had their worst week since January 2016 with a heavy sell off that sent the Dow nearly 12% below it’s January highs, falling 5.7% on the week ending at 23533. The Dow is set for it’s worst performing quarter sine Q3 2015. The S&P gave back over 2% on Friday, ending the week at 2588 just off the daily low of 2585, which is also the 200 day moving average.

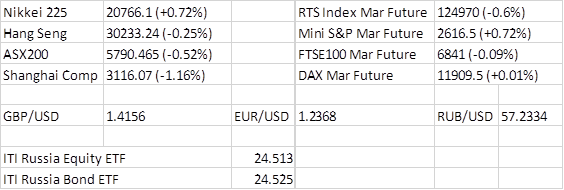

The major Asia-Pacific indices started the week on the back foot, but moved off of lows as US index futures ticked higher. - Japan's Nikkei 225 lost around 0.4% as electronics names continued to flounder, with the utilities sector leading the way lower, althoughy stocks have rallied towards the European open with the index closing 0.7% to the good.. Health care names outperformed, while consumer staples also trod higher. - The Hang Seng shed 0.5%. The mainland CSI 300 has lost around 1.4%. Chatter on Friday suggested that state funds intervened amid the market freefall, with similar murmurings from some quarters suggesting the same happened today. - Australia's ASX200 lost 0.5%. - US index futures edged higher with reports of a slightly softer US-China trade backdrop & an agreement on trade matters between the US & South Korea. The e-mini S&P future added 20 points, while mini Dow futures added 160 points.

TREASURIES: Friday provided a relatively quiet end to a hectic week, with Tsy futures mildly higher by the closing bell, seeing a late rebound as equities resumed their slide. 3-Year Bond futures are back from session highs, last trading at 97.845 (+0.5 tick), while 10-Year Bond futures last trade at 97.340 (unch.) - The domestic 3-/10-Year yield is last 0.6bp steeper at 56.5bp, while the AU/US 10-year yield discount has widened by around 1.7bp to 16.8bp. - 3-month BBSW fixed 0.5bp higher today, at 2.00%, which has led to IRM8 & IRU8 trading 1 tick softer, while the remainder of the white & red contracts are unchanged to a tick higher. - It will be a light week for the domestic economic docket, curtailed by the Easter holiday.

OIL: Crude initially ran higher as Saudi Arabia intercepted Yemeni launched missiles over Riyadh, although both WTI & Brent crude futures moved into negative territory, with no real news flow present. - WTI last traded $0.30 or so lower at $65.55, while Brent lost around $0.25 to trade at $70.20. - The Middle East tensions initially outweighed Friday's uptick in the weekly Baker Hughes rig count data before WTI ran out of steam in front

of the 2018 high of $66.66, topping out at $66.55.

GOLD: Gold consolidated Friday's gained, sticking to a tight range, last at $1,348/oz in spot dealing.

FOREX: The USD was softer against the bulk of its major counterparts, with the JPY proving to be the only notable exception to the rule. JPY crosses were driven higher by AUDJPY demand that was attributed to Japanese banks, with the AUD outperforming as a result. USDJPY last traded at 104.90, off of the 105.06 highs, while AUDJPY traded at 81.10. Traders may look to the $1.19bln worth of 105.00 option expiries at the 10AM NY cut later today. - AUDUSD trod higher as a result of AUDJPY demand, last trading 30 points better off at 0.7730, while NZDUSD neared the 55-DMA at 0.7285, trading 40 pips higher at 0.7275. The RBNZ's new PTA was formally announced this morning, and confirmed that the central bank is now expected to contribute to supporting "maximum sustainable employment" alongside its medium term inflation target. The committee based decision making that was also expected was formalised and will go into play in 2019. On the economic docket New Zealand's February trade balance printed a surprise surplus. Elsewhere EUR, GBP & CAD moved higher against the greenback, trading in familiar territory, while CHF's gains vs. USD were more measured. Fedspeak provides the main risk event on Monday.

For information on ITI ETFs visit itifunds-etf.com

For institutional sales & trading please contact Steve Farrell

For all dealing enquiries please contact our Trading Desk